In the ever-evolving landscape of tax compliance, one might expect flexibility to accommodate the diverse realities of self-employed individuals. Yet, Garry Piccolo finds himself ensnared in a paradoxical bind: he is required to adhere to Making Tax Digital (MTD) regulations even though his rental income barely registers at £3,680. His total income, including other earnings, surpasses £52,000—placing him squarely in HMRC’s crosshairs.

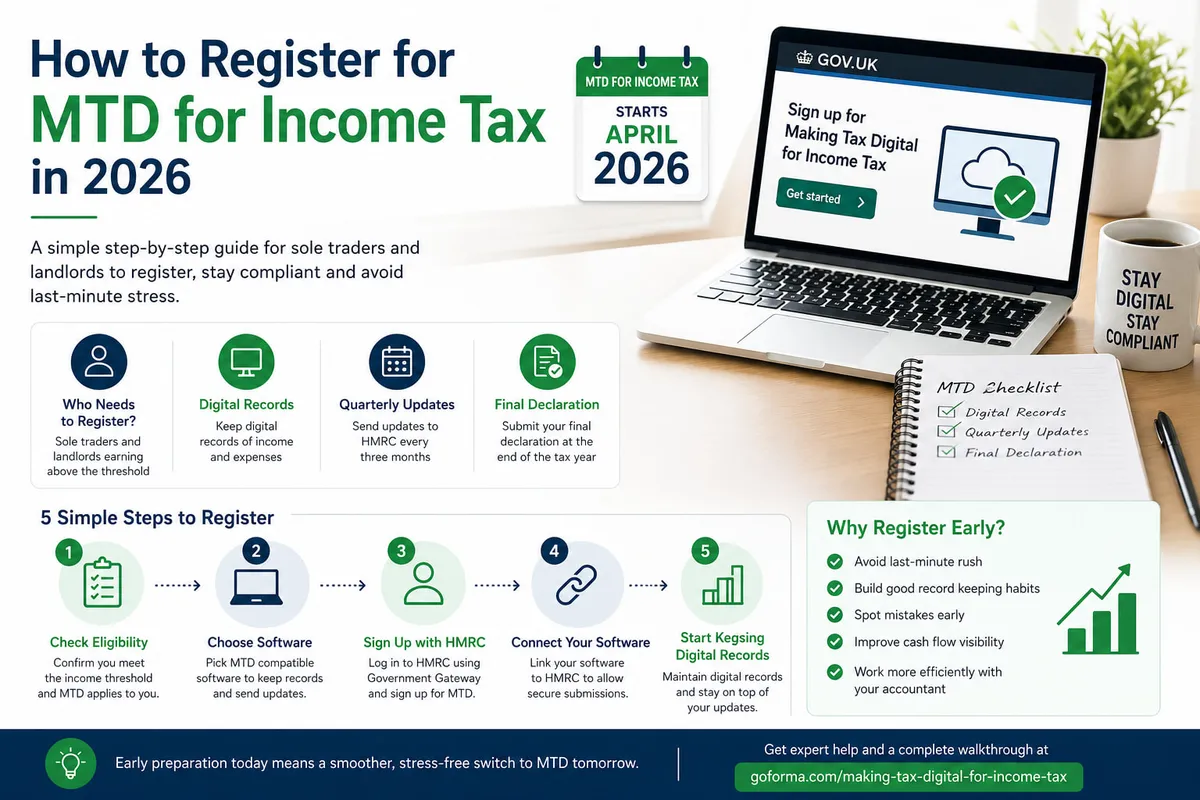

Making Tax Digital for Income Tax is a UK government initiative designed to transition tax reporting into the digital realm. The aim is clear: streamline processes and enhance compliance through real-time reporting. But for many, including Piccolo, this shift feels less like progress and more like an imposition.

As of April 2026, MTD will apply to individuals earning over £50,000 from business or property income. By April 2027, this threshold will drop to £30,000. For Piccolo, the implications are stark; while he earns well below these limits in rental income alone, his overall earnings necessitate compliance.

“It’s ridiculous,” he states emphatically. “The Government says it’s making things easier for the self-employed, but everything you do brings another cost.” Indeed, Piccolo faces accountancy fees nearing £2,500 just to navigate the complexities of MTD compliance.

Under current regulations, taxpayers can only exit MTD once their qualifying income dips below the threshold for three consecutive years—a stipulation that further complicates matters for those with fluctuating incomes. Michelle Denny-West articulates this rigidity: “Liability is decided by income levels in 2024-25 and, unless a taxpayer’s MTD qualifying income stops entirely, subsequent changes in circumstances count for nothing.”

This stringent framework raises questions about how it serves small business owners who are often at the mercy of unpredictable market conditions. Richard Creedon notes that while technology abounds in accountancy practices—“It’s not that there’s not enough technology in the boardroom,” he says—it remains disconnected and fragmented.

The transition to digital tax reporting seems poised to benefit larger firms equipped with resources but leaves smaller traders grappling with additional burdens. As MTD rolls out further over the next few years, observers anticipate increasing frustration among those caught in its web.

For now, Garry Piccolo must prepare for five tax submissions each year under MTD—an arduous task that looms over him like a cloud of uncertainty. The reality is stark: even those earning modest incomes are not exempt from the sweeping changes aimed at modernizing the UK tax system.